HRA is covered under Section 10(13A) of Income Tax Act 1961. Salaried Employees who live in a Rented house can claim HRA to lower their taxes – partially or wholly. The decision of how much HRA needs to be paid is made by employer. Part of Salary is apportioned to HRA.

1. CONDITIONS FOR CLAIMING HRA EXEMPTION?

– Salaried Individual only can claim HRA.

(Self employed cannot claim HRA. However Self Employed can also claim deduction of Rent paid under Section 80GG of Income Tax Act 1961.)

– Stay in Rented Accommodation

(Not living in a self owned).

– Rent paid exceeds 10% of Salary.

– HRA is a part of Salary.

(Can be seen in Form 16(B) Sr.no. 2 (e).)

– Not paying rent to spouse.

2. HOW MUCH DEDUCTION CAN BE TAKEN?

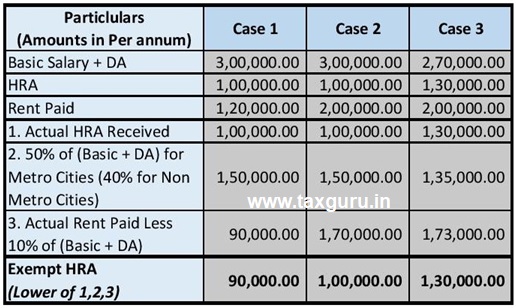

Deduction available is least of the following:

i. Actual HRA Received.

ii. 50% of (Basic salary + DA) for living in Metro Cities (40% for Non Metro Cities).

iii. Actual Rent paid less 10% of Basic Salary + DA

Let us understand with the help of some Examples below:

3. DOCUMENTATION IN CASE OF SUBMITTING PROOF TO EMPLOYER?

1st: Rent Receipt provided by the Landlord.

Note: If Total Annual Rent paid is more than Rs. 1,00,000/- than PAN

Number of Landlord is Mandatorily to be mentioned.

(If PAN Number is not provided by the Landlord then take a Declaration from the landlord of not holding the PAN Number).

2nd: Rent agreement should be furnished if demanded by the employer.

3rd: It is always advisable to pay rent by Cheque or by electronic payment mode.

4. Can Mr. XYZ claim HRA by paying rent to family members?

YES! HRA can be claimed by paying Rent to Parents.

Following steps needs to be taken:

Please Note: That HRA cannot be claimed by paying rent to spouse.

5. FREQUENTLY ASKED QUESTIONS?